Development News

September 2014

Development is proceeding in a number of directions

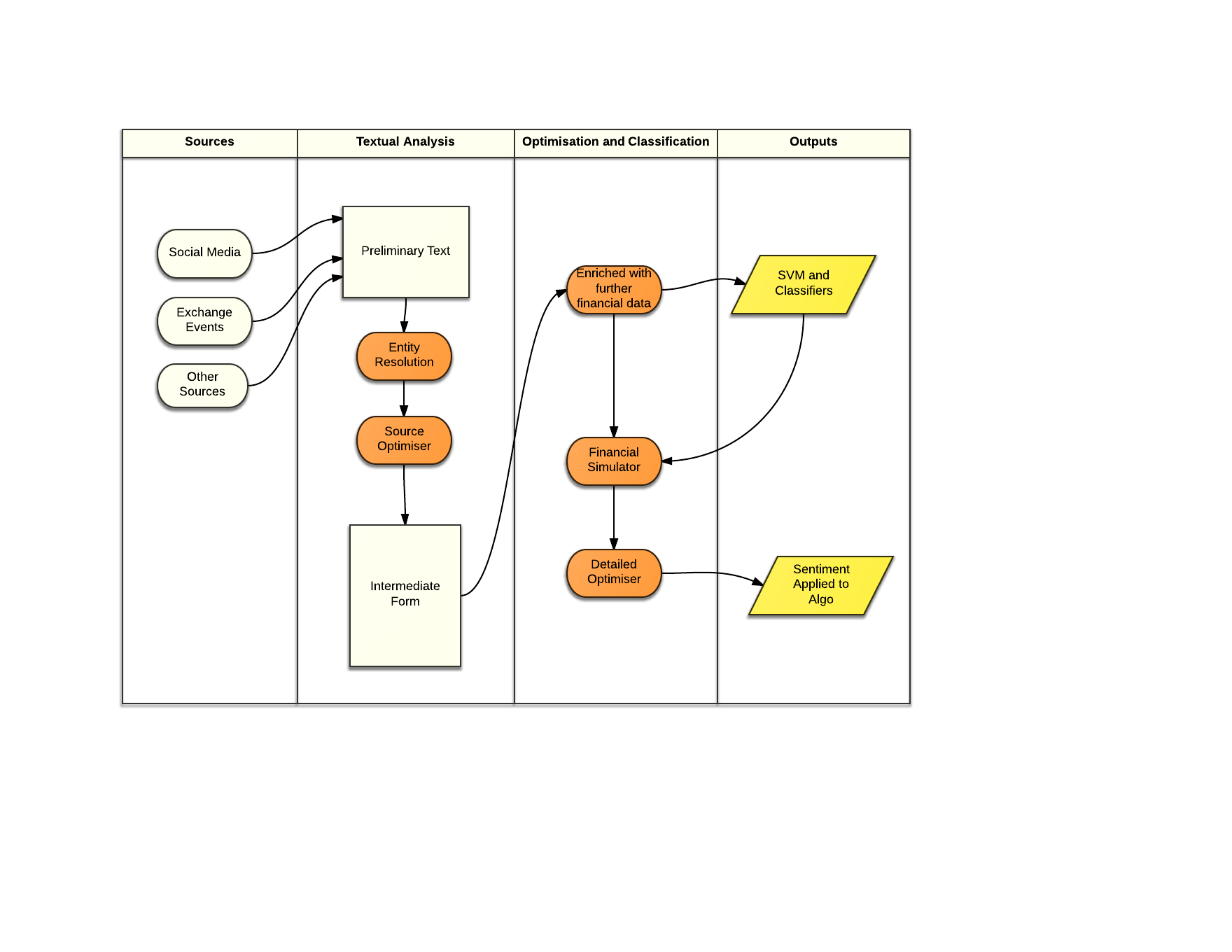

We are currently re training the Stanford NLP with our own data , this is a laborious process taking thousands of sentences and applying sentiment values to them

Once that is done there will be extensive testing against the corpus I have been collecting, then further analysis against various financial parameters

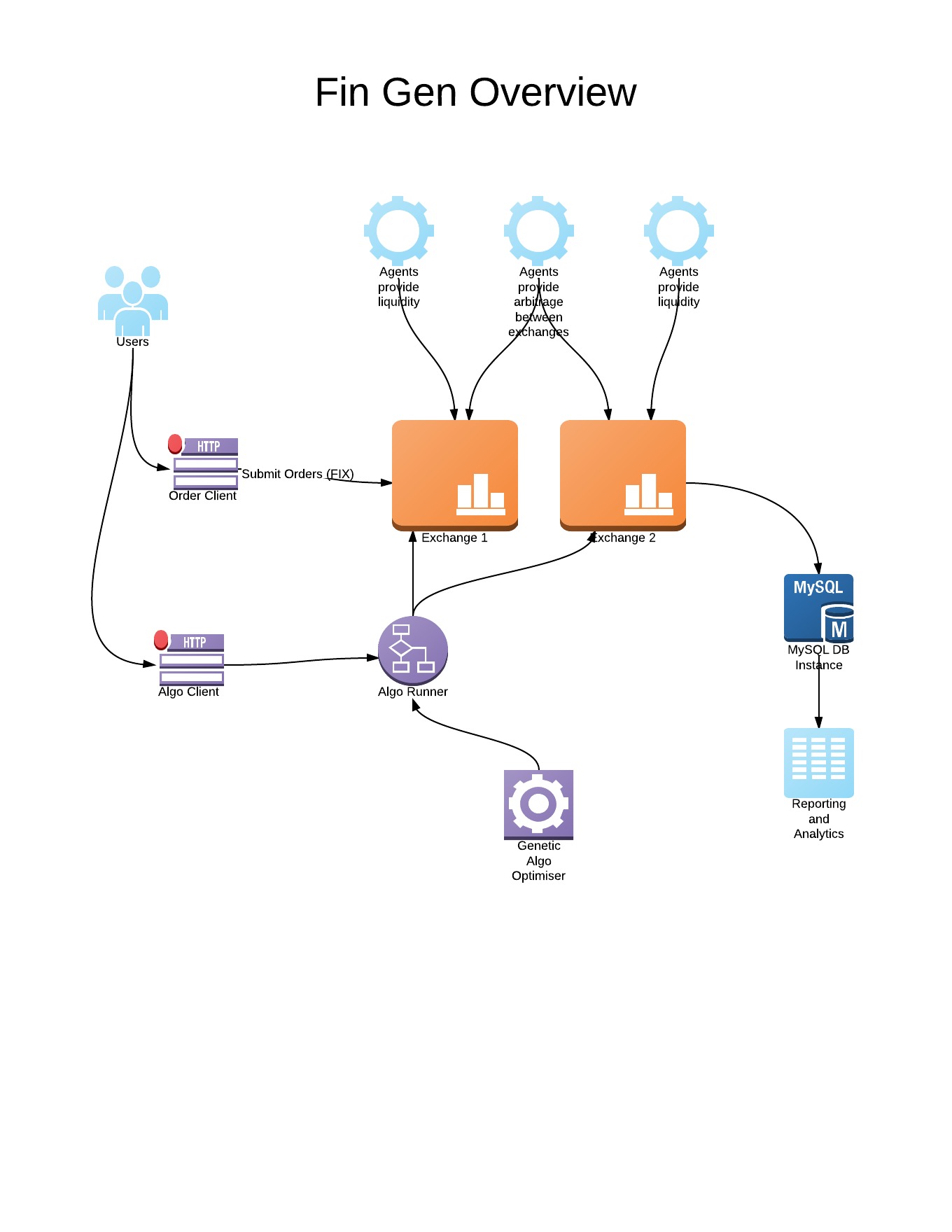

Development has also started on a machine learning framework to analyse both textual data from twitter and time series data from the markets and the simulator.

In addition to the FIX based messages we will be introducing messaging based on the Simple Binary Encoding Format Simple Binary Encoding Format to improve latency when translating messages.

June 2014

The matching engine is finished and the simulator is up and running on its new host.

March / April 2014

Coding of the matching engine is almost complete, enough to produce background orders. Once the various clients have been wired back into the application you will be able to send in orders and set up portfolios.

The previous server has been retired and we are on a temporary host until a better hosting solution is found.

October 2013

A great refactoring of the matching engine (virtually a rewrite) to produce better performance, particularly with concurrency in mind.

June / July 2013

The first iteration of the genetic programming side has been completed there is a general framework with a couple of specific implementations of decision making features : - a simple virtual machine and a simple neural network.